Key points of interest:

- Offshore wind is the key driver behind the global wind power generation - just 8 years are needed to reach the next 1-terawatt (TW) mark v.s. 40 years to reach the first 1TW.

- Why we see last year’s muted offshore wind market will be short-lived?

- Why biodiversity risk should not be underestimated?

|

|

Target 7.2 By 2030, substantially increase the share of renewable energy in the global energy mix |

- Theory of change - Faster offshore wind deployment enabled by cost-competitive technologies and essential services is critical to successful energy transition.

- Expected positive impact - Significant green-house gas (GHG) reduction over product life cycle (actual outcomes vary by area and region). In the EU, the net benefit from offshore wind is estimated to be over 220g GHG reduction per kwh electricity production.

- Potential negative impact and risks: biodiversity (birds, bats and marine fauna species, habitats, marine ecosystems), conflicts on ocean-use, end-of-life waste and water.

How we invest in the theme

6.1% of Espiria SDG Solutions portfolio has significant exposure to the offshore wind market (as of 5 June 2023).

The market plays a unique role in a successful green energy transition.

- Better market environment entering 2023, with less cost pressure, better investment return, higher policy certainties and a large pipeline of upcoming project auctions in Europe and China.

- Significantly positive life-cycle impact for our investments. Green-house gas (GHG) per unit of electricity generated from offshore wind is location dependent, but it can be as low as 5-10 g/kwh, in contrast to 238g/kwh which is the average level of GHG intensity of electricity generation in the EU as of 2021.

- We invest in selective sweet spots on the offshore wind value chain. Global offshore project development, high-spec large turbine installations and services, Chinese wind turbine leaders with offshore edge.

Lately, we are delighted to see positive development on turbine blade recycling options. A new chemical process discovered as part of a Vestas-led project can make all current wind turbine blades recyclable, removing the need for changing the design or the composition of the material used. It allows for epoxy-based blades to be broken down into raw material that can be reused to make new wind turbine blades or other purposes.

On the other hand, we also took on more cautious views on the complexity of biodiversity risk assessment around offshore wind development, after speaking with several stakeholders in the industry.

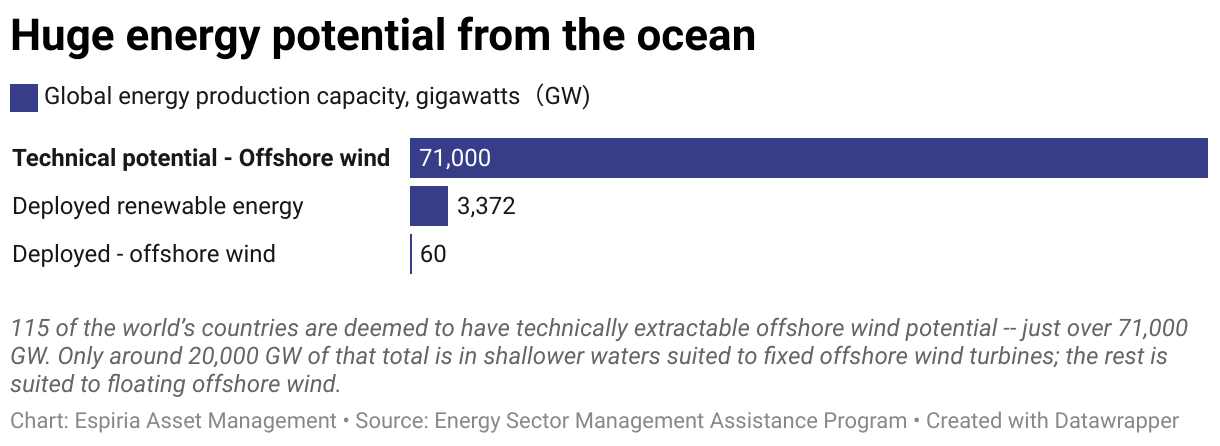

The wind industry is at the dawn of reaching a milestone - the global wind power generation capacity will likely pass the one-terawatt (TW) bar for the first time by the end of 2023, a mark that took 40 years to reach. However, to reach the next terawatt milestone, only 8 years is needed, according to the latest market outlook from energy research and consultancy company Wood Mackenzie. Onshore wind turbine technology advancement and economies of scale were key drivers behind our last TW milestone, but what will drive an acceleration towards the next one? The large-sized blades spinning on Earth's vast ocean surface is the simple answer, the so-called offshore wind turbines, either with their bottom fixed to the seabed or anchored on floating structures. In the vision of an energy supply that never runs out, unlike fossil alternatives, offshore wind deserves a place. When considering only suitable wind speed and water depth, the technical potential of offshore wind is over 71 terawatts, 20 terawatts in shallower waters suited for bottom-fixed offshore wind turbines and the rest for floating ones.

Although wind power only generates around 1% of the world's electricity today*, the International Energy Agency (IEA) believes it will play a significant role in the coming two to three decades - by the time today’s children reach their prime years in life.

By 2030, about 15% of global electricity demand will be fulfilled by wind power and 25% by 2050. Those who live in the EU, will see an even larger impact from wind power, as the EU moves towards an electricity system dominated by wind, accounting for just over 40% of total generation in 2050**. Offshore wind power, delivered by the large-sized turbines anchored on the seabed often less than 50 meters below and within a 60km distance from shore, is the critical technology which will turn such high hopes into reality.

Wind turbines located at sea often take on higher and more consistent wind speeds, the farms can also be larger than onshore installations, leading to potentially greater power output and efficiency than other renewable energy technologies. Besides, being located far from populated areas, offshore wind farms generally have less impact on people in terms of noise and visual disturbance than onshore turbines. On the other hand, offshore wind installations often incur higher costs related to installation and maintenance, and the grid connection to offshore wind farms can be technically challenging and costly. However, its overall cost competitiveness has already been proven, particularly in areas where wind sources are abundant, such as in Europe.

Europe has the biggest cost advantage so far in installing offshore wind farms. When measured by average cost per unit of electricity generated over an offshore wind turbine's life cycle, often referred to Levelized Cost of Electricity (LCOE), the numbers speak for themselves. According to IEA, EU offshore LCOE was $60 per megawatt hours (MWh) in 2021, far superior to fossil alternatives in the region, which were running at LCOE between $140-180/MWh prior to the recent European energy crisis. As technologies further mature and offshore infrastructure expands, the LCOE of EU offshore is expected to further decline to $40/MWh by 2030 - cheaper than onshore wind, and to $30/MWh by 2050 - a level on par with Solar PV in the same region. Globally, the cost of EU offshore wind energy remains competitive. It is currently 50% lower than the US and Indian averages and 40% lower than the average cost in China***.

In practice, the attractiveness of an offshore wind farm depends heavily on its location, with its specific wind resources and seabed conditions, as well as factors such as local economic conditions and energy policies. Because of this, the unit cost of an offshore wind farm can vary greatly from one project to another. Nevertheless, the underlying trend of declining renewable energy development costs applies also for offshore wind. If the IEA is right in its forecast, offshore wind will become a cheaper power generation source than fossil alternatives also in the US and China by 2030, and in India by 2050. The pace at which this takes place depends on the cost of capital, improvements in technology and operational costs.

At the end of 2022, the world deployed around 60 gigawatts (GW) of offshore wind capacity, despite a somewhat disappointing year, during which offshore installations and investments took a hit due to multiple factors: a subsidy phasing-out effect in the Chinese market, rising interest rates, inflation, and a highly uncertain regulatory environment in Europe. New investors deemed “waiting” was a better strategy amid uncertainties, but this can change quickly.

Entering 2023, the offshore industry is ready to reignite its engine again. A number of larger auctions are planned in the second half of the year. A few countries are launching their first offshore auction this year, including Ireland and Portugal (among others), both are large in scale. Bloomberg NEF estimates that an average of 30 GW offshore wind capacity is to be built each year until 2030 - a major step-up from its historical deployment pace. Does this outlook appear hefty? Not at all if one believes in the ambitious targets announced by leading countries. Many governments see an accelerated offshore market as politically attractive, as it often has high public acceptance, potential for sizable direct investment, job creation and local economic development.

Various regional cooperations make national targets more convincing. Without regional cooperation, individual governments might be tempted to create markets independently, building supply and value chains that may lack economies of scale.

European countries are at the forefront. In late April 2023, nine European countries (including the UK, Germany, Netherlands, etc.) signed a collective target to make the North Sea the “green power plant of Europe”, coined as the Ostend Declaration, and set to have at least 120 GW of offshore wind energy capacity installed by 2030, and at least 300 GW by 2050. Eight countries in the Baltic Sea have now committed to increase that to 19.6 GW by 2030, with a plan to consider a 2040 target at a later stage. China, who overtook the UK as the largest driving force on the global offshore wind scene in 2021, has all incentives to continue to do so to achieve its carbon peaking and carbon neutrality goals set by 2030 and 2060 respectively, dubbed as Dual Carbon Goals. Even the US, a country where offshore wind deployment is close to zero today, has set a bold goal of deploying 30 GW of offshore wind by 2030 under the Biden administration. Several factors hindering its offshore wind progress have become less of an issue today. Europe has shown the way for cost reduction; state and federal support stepped up, and more people see that integrated planning of using ocean resources can be a way out to resolve historical opposition from a coalition of stakeholders – mainly commercial fishermen and coastal landowners who don’t want turbines spoiling their views.

Apart from setting ambitious goals, the EU commission has also taken actions to address key bottlenecks in renewable development. The offshore wind projects, often characterized by 5 to 10 year-long development cycle, are sensitive to the ease of bottlenecks such as obtaining permits faster, grid connectivity and electricity market reform. The European Commission made the electricity market reform proposals in March of this year, which focused on incentivising longer-term contracts with an aim to decouple the electricity bill from short-term market prices. Concrete proposals include introducing measures to boost the uptake of Power Purchase Agreements (PPAs), requiring member states, among other things, to support lowcarbon power generation only in the form of two-way Contracts for Differences (CfDs). While these measures do not affect how short-term electricity prices are formed, it does change the way infra-marginal power generators are remunerated, and that it should enhance the stability and predictability of electricity costs across the EU, as seen by the EU Commission. Investment certainty increases with improved markets for long-term contracts, lowering perceived financial risk.

While regulatory changes rapidly accelerate, other areas can take a longer time to improve. One example is the time needed to ensure accurate assessment of biodiversity risks. In recent dialogues with some key stakeholders involved in the offshore wind industry, we came back thinking an investor should not underestimate the complexity in assessing biodiversity risks related to offshore wind build-out, especially in areas where biodiversity loss has already occurred, such as the Baltic Sea. WWF Baltic Ecoregion Programme (WWF BEP) and Coalition Clean Baltic (CCB), as environmental NGOs, highlighted in their recent report**** the current lack of data and science gaps related to potential on-site and cumulative impacts into already heavily pressured ecosystems in the Baltic Sea. The NOG further points out the urgency to consider cumulative and compounding impacts from multiple offshore renewable energy projects, multiple sectors from one or several countries and time overlapping. This puts close collaboration among stakeholders in the spotlight, where integrated planning, an inclusive approach and conflict resolution mechanisms can all play a key role.

New opportunities do exist if stakeholders collaborate closely and successfully implement integrated planning. Actions such as developing cross-border wind-farm interconnections, adopting dual-purpose underwater cables, and Power-to-X applications can reduce environmental impacts in general. One wind developer pointed out that unused energy from offshore turbines paired with hydrogen electrolyser can potentially re-inject oxygen into the seabed, helping to restore marine biodiversity. The offshore wind turbine infrastructure can possibly even host military monitoring systems. In a dynamic ecosystem comprised mainly of ocean and the air above, fully understanding the impact from large wind turbines requires time and proactive work. If anything is missed, the time needed to restore the condition of nature can be decades.

*IEA report, https://www.iea.org/reports/wind-electricity

**Based on stated policy scenario, World Energy Outlook 2022, IEA

***The White House press release

****Guidelines for planning offshore renewable energy in the Baltic Sea, Summary report 2023, Coalition Clean Baltic, WWF